At first glance, the domain market appears disordered.

A five-letter .com sells for $3,000, while another—nearly identical—changes hands for $75,000. A one-word domain trades for seven figures, while dozens of comparable words remain unsold for years. To most observers, this looks like inconsistency, even irrationality.

But this impression is false.

What appears as randomness is, in reality, structure without visibility. The domain market is not chaotic. It is simply incompletely understood. Beneath the surface, it follows a set of statistical and linguistic laws that are both consistent and measurable—once one knows where to look.

The most important of these laws is also the least recognized: domain prices do not follow a normal distribution. They follow a heavy-tailed distribution, a power-law system in which a small number of transactions account for a disproportionate share of total value. This is not a minor technical detail. It is the defining feature of the market.

Across decades of observed domain transactions, a consistent pattern emerges. The overwhelming majority of domains transact at relatively modest prices, while a very small minority account for the largest share of economic activity. This asymmetry is not unique to domains—it appears in venture capital, equity markets, real estate, and even cultural markets such as books or art. But in domains, the effect is particularly pronounced because of the nature of the underlying asset.

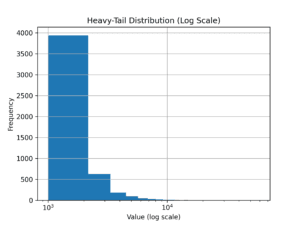

The Shape of the Market

Domain price distributions exhibit a heavy-tailed structure, where most transactions cluster at lower values while a small number define the upper range of the market.

When visualized on a logarithmic scale, the structure becomes immediately visible. Prices cluster heavily in the lower ranges, while the right tail extends dramatically into higher-value territory. The distribution is not symmetric; it is skewed, elongated, and decisively non-linear.

This has immediate consequences for how the market must be interpreted. Averages become misleading because they are pulled upward by a small number of extreme values. Medians, while more stable, fail to capture where most of the economic significance lies. The so-called “outliers” are not statistical anomalies—they are the market. They define its shape, its incentives, and its long-term behavior.

To understand why this structure exists, one must move beyond price data and examine the underlying drivers of value.

The first is linguistic scarcity. While millions of domain names are technically possible, only a very small subset possesses the qualities that the market consistently rewards: brevity, clarity, recognizability, and semantic precision. Language, in economic terms, is not abundant—it is highly uneven. Certain words carry disproportionate meaning, and meaning is what markets ultimately price.

The second driver is economic leverage. A premium domain is not merely a digital identifier; it is a strategic asset. It can reduce customer acquisition costs, increase trust, improve conversion rates, and establish immediate authority in a given market. Its value therefore scales with the success of the business built upon it. This creates non-linear valuation. The difference between a good domain and a great one is not incremental—it is multiplicative.

The third factor is timing. Markets do not price potential immediately. They price what is recognized, understood, and narratively validated. This introduces a delay between intrinsic value and observed price. When recognition eventually occurs, the adjustment is not gradual—it is abrupt. Prices move in discrete steps rather than smooth progressions.

These forces—linguistic scarcity, economic leverage, and delayed recognition—combine to produce the heavy-tailed structure observed in domain pricing.

The Hierarchy of Value

![]()

When ranked by price, domain sales follow a power-law pattern, highlighting the exponential gap between top-tier assets and the broader market.

A second way to understand the market is through rank. When domain transactions are ordered from highest to lowest price, the resulting curve reveals the same underlying geometry. The highest-priced domains are extraordinarily rare, and value declines sharply as rank increases. The relationship is not linear—it follows a power-law pattern, where a small number of assets dominate the entire structure.

This has profound implications. The difference between the very top of the market and everything below it is not marginal—it is exponential. Yet most participants continue to approach the domain market as if it were linear. They assume that small differences in quality should produce small differences in price. This assumption is fundamentally flawed.

In a power-law system, small differences in quality can produce massive differences in outcome.

Consider domains that appear nearly identical at first glance. Minor variations in spelling, rhythm, or semantic clarity can result in vastly different valuations. One name aligns perfectly with linguistic expectation and market intuition. Another introduces subtle friction. A third fails to convey meaning effectively. The resulting price differences are not arbitrary—they are the natural consequence of nonlinear valuation.

Beyond the Illusion of Liquidity

This leads to a deeper understanding of the domain market’s structure. It is not a flat marketplace in which assets are distributed evenly across a spectrum of value. It is a hierarchical system.

At the top sits a very small group of domains that define the market’s economic reality. Below them is a broader tier that participates in value formation. And beneath that lies the majority of domains, which provide liquidity but not lasting value.

This distinction between liquidity and value is essential. Liquidity refers to how frequently assets trade and how easily they can be exchanged. Value refers to their long-term economic impact. In heavy-tailed systems, these two concepts diverge sharply. The most frequently traded assets are rarely the most valuable. High-value assets often trade infrequently, precisely because their worth is not easily agreed upon or immediately recognized.

Time, therefore, becomes a structural variable. Because value is concentrated and recognition is delayed, patience is not simply a strategic choice—it is a requirement. Most domains will never reach extreme valuations, but those that do often require years before the market fully understands them. The largest gains occur not at acquisition, but at recognition.

Implications for Investors, Founders, and Institutions

For investors, this shifts the objective entirely. Success does not come from broad diversification across average-quality assets. It comes from concentrated exposure to structurally strong names—those aligned with linguistic clarity, economic utility, and future demand. The discipline lies not in activity, but in selection and patience.

For founders, the implication is equally clear. A domain is not a cosmetic decision. It is an infrastructural one. The right name reduces friction across every layer of a business, from marketing efficiency to customer trust. The wrong name imposes a persistent cost—one that compounds over time and rarely appears explicitly on financial statements.

For institutions, the domain market remains largely uncharted. It is under-institutionalized, under-analyzed, and therefore inefficient. But this inefficiency is temporary. As data becomes more transparent and analytical frameworks become more standardized, pricing dispersion will narrow, and capital allocation will increase. Domains will gradually transition from a fragmented marketplace into a recognized asset class.

From Noise to Structure

Every asset class follows a similar path: fragmentation, price discovery, standardization, and eventual institutionalization. Domains are currently positioned between discovery and standardization. The structure is already present. What is missing is widespread recognition.

The persistent belief that domain pricing is inconsistent or unpredictable stems from a misunderstanding. The market is not random. It is governed by identifiable laws—statistical, linguistic, and economic. These laws are not immediately obvious because they are nonlinear and require disciplined analysis to uncover. But once understood, they provide a coherent framework for interpreting market behavior.

What appears to be noise is, in reality, unmeasured structure.

The domain market does not reward activity. It rewards alignment—with language, with meaning, and with the underlying geometry of value itself. Those who recognize this no longer see randomness. They see pattern, hierarchy, and inevitability.

And once that structure becomes visible, the market no longer appears unpredictable.

It appears exact.