Liquidity Does Not Mean What You Think

Markets are judged by activity.

Volume is interpreted as health. Turnover is treated as validation. A market that trades is assumed to be functioning; one that does not is assumed to be failing.

This assumption is rarely examined.

Liquidity does not describe value. It describes movement. The two are not equivalent.

In the secondary domain market, this distinction is critical.

Domains are not traded instruments. They are stored capital.

Stored capital does not move continuously.

Most of the Market Does Not Trade

The defining characteristic of the domain market is not activity, but inactivity.

The majority of domains never transact. Turnover is low, irregular, and highly selective.

Your own data shows:

- Annual turnover: approximately 1%–4% of the asset base

- Holding periods: frequently measured in years, not months

This places domains structurally closer to:

- fine art

- commercial real estate

- collectible assets

…than to equities or commodities.

Liquidity is therefore not a baseline condition. It is an event.

What You See Is Not the Market

Public data creates a false sense of completeness.

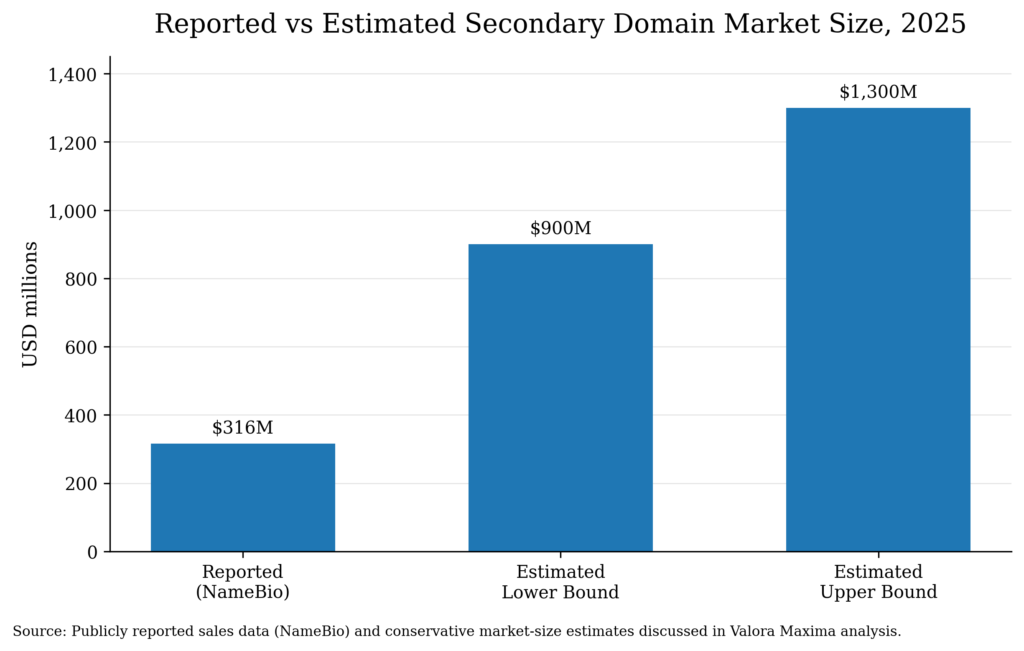

In 2025:

- ~190,000 publicly reported transactions ≥ $100

- ~$316 million in visible transaction value

Yet estimated total market size is:

- ~$900 million to $1.3+ billion

The visible layer is not the market. It is a subset.

More importantly, it is a biased subset.

High-value transactions are disproportionately:

- private

- brokered

- non-disclosed

The highest-quality price signals are often absent from the dataset.

Liquidity appears where visibility exists—not where value is concentrated.

Liquidity Is Layered, Not Uniform

The domain market is not homogeneous. It is structurally segmented.

At minimum, three layers exist:

- .COM+ — core capital layer

- Tech extensions — cyclical growth layer

- Regional domains — localized stability layer

Each exhibits distinct liquidity characteristics.

.COM

- deepest liquidity

- strongest end-user demand

- lowest structural risk

Tech

- high turnover

- sentiment sensitivity

- strong correlation with venture cycles

Regional

- stable but constrained

- tied to domestic adoption

Liquidity is not evenly distributed. It is hierarchical.

Liquidity Is Often a Function of Replaceability

Modern markets overvalue activity.

High liquidity is assumed to indicate importance. In practice, it often indicates substitutability.

Assets that trade frequently are typically:

- standardized

- replicable

- interchangeable

Illiquid assets, by contrast, tend to be:

- specific

- constrained

- difficult to replace

Domains fall into the latter category.

A strong domain is not easily substituted. Its liquidity is therefore conditional, not continuous.

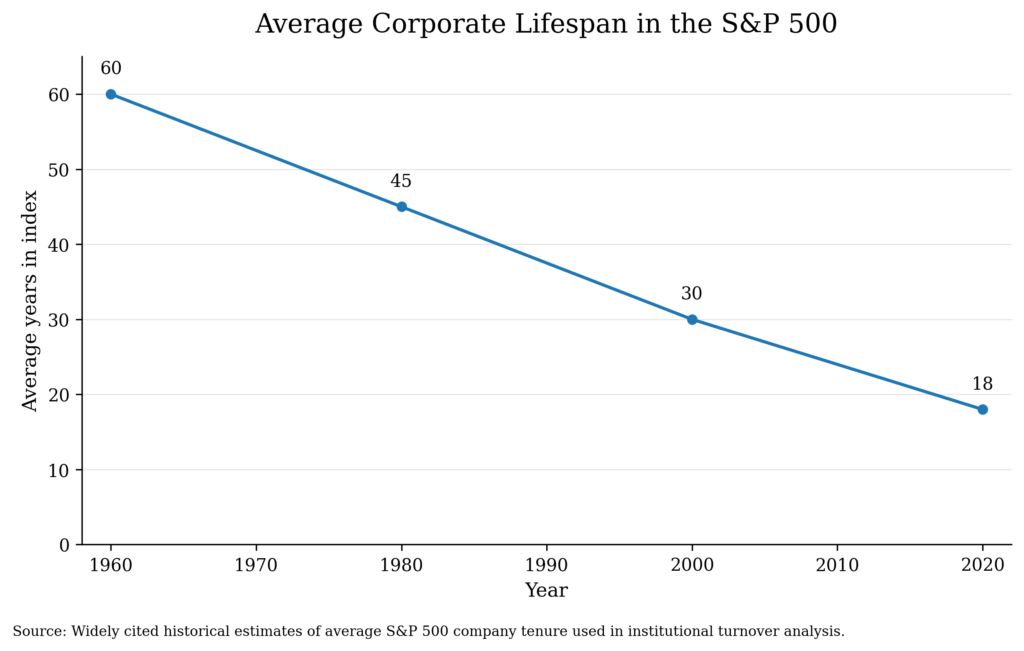

- ~60 years (1960)

- <20 years (2020)

Corporate turnover has accelerated dramatically.

This reflects increasing:

- competition

- disruption

- replaceability

Companies are transient. Their identities evolve, merge, or disappear.

Domains do not behave this way.

Domains Accumulate Meaning

A domain is not a product. It is a fixed linguistic asset.

Its value is not derived from:

- production

- output

- operational performance

It is derived from:

- memorability

- clarity

- semantic positioning

Unlike companies, domains:

- do not degrade operationally

- do not require reinvention

- do not compete in the same dynamic

They accumulate meaning over time.

Liquidity follows meaning—not the reverse.

Price Discovery Is Discontinuous

In most markets, price discovery is continuous.

In domains, it is episodic.

There is no:

- centralized exchange

- standing bid

- continuous pricing mechanism

Transactions occur only when:

- a specific buyer

- with a specific need

- encounters a specific asset

This creates:

- wide dispersion in observed prices

- long periods of inactivity

- sudden transaction clustering

Liquidity is therefore not a function of time.

It is a function of alignment.

Liquidity Appears in Windows

Because of this structure, domain liquidity concentrates in windows.

Examples include:

- startup funding cycles

- sector expansion (AI, crypto, etc.)

- corporate rebranding phases

During these periods:

- buyer urgency increases

- capital is deployed

- transaction frequency rises

Outside these windows:

- activity declines

- price signals become sparse

The market does not disappear.

It becomes latent.

Capital Allocation Is Implicitly Structured

Your own framework reflects this clearly.

The domain market behaves like a portfolio:

- .COM → core capital preservation

- Tech → growth allocation

- Regional → stability and diversification

This is not explicit portfolio construction.

It is emergent behavior.

Participants allocate capital according to:

- perceived durability

- expected liquidity

- narrative momentum

Liquidity is the outcome of this allocation—not its driver.

Why Liquidity Misleads

The core misunderstanding is simple:

Liquidity is interpreted as evidence of value.

In reality, it is often evidence of:

- accessibility

- standardization

- narrative alignment

Domains invert this relationship.

The most valuable domains:

- trade infrequently

- require specific buyers

- command attention only under the right conditions

Low liquidity is not a weakness.

It is a characteristic of constrained supply.

The Role of Time

Time is the dominant variable in domain valuation.

Not calendar time, but:

- adoption time

- recognition time

- commercial alignment time

These processes are:

- slow

- uneven

- irreversible

A domain does not become valuable because it trades.

It trades because it has become valuable.

Implications for Market Participants

The practical conclusion is straightforward.

Liquidity should not be pursued.

It should be interpreted.

What matters is not:

- how often an asset trades

- how visible its price is

But:

- whether it can eventually attract the right buyer

This depends on:

- linguistic quality

- commercial relevance

- structural positioning

Liquidity is the endpoint—not the starting point.

The Valora Maxima Perspective

The Valora Maxima Domain Index is designed to measure:

- structural price behavior

- not transactional noise

This requires:

- smoothing mechanisms

- outlier control

- length-based normalization

The goal is not to track liquidity.

It is to isolate:

underlying price structure across the asset class

Because structure persists.

Liquidity fluctuates.

Conclusion

Markets reward what moves.

But movement is not value.

In domains, the opposite is often true.

The assets that matter most:

- move rarely

- trade selectively

- accumulate meaning over time

Liquidity, in this context, is not a signal of strength.

It is a byproduct of alignment.

Understanding that distinction is the difference between:

- participating in the market

- and understanding it